Anthropic vs. the Three Competitive Axes

1. The MCM Lens on Competition

MCM does not treat competitors as a flat list. The method structures competition through three interlocking lenses:

M4 (Economic Value): What kind of value does each player sell? Commodity → Products → Services → Experience. This determines the nature of the competitive fight.

M9 (Value Map): How does each player perform on the market's Key Expected Benefits? This determines who wins the customer at the moment of decision.

Archetype: What strategic machinery is each player running? This determines whether they are even playing the same game.

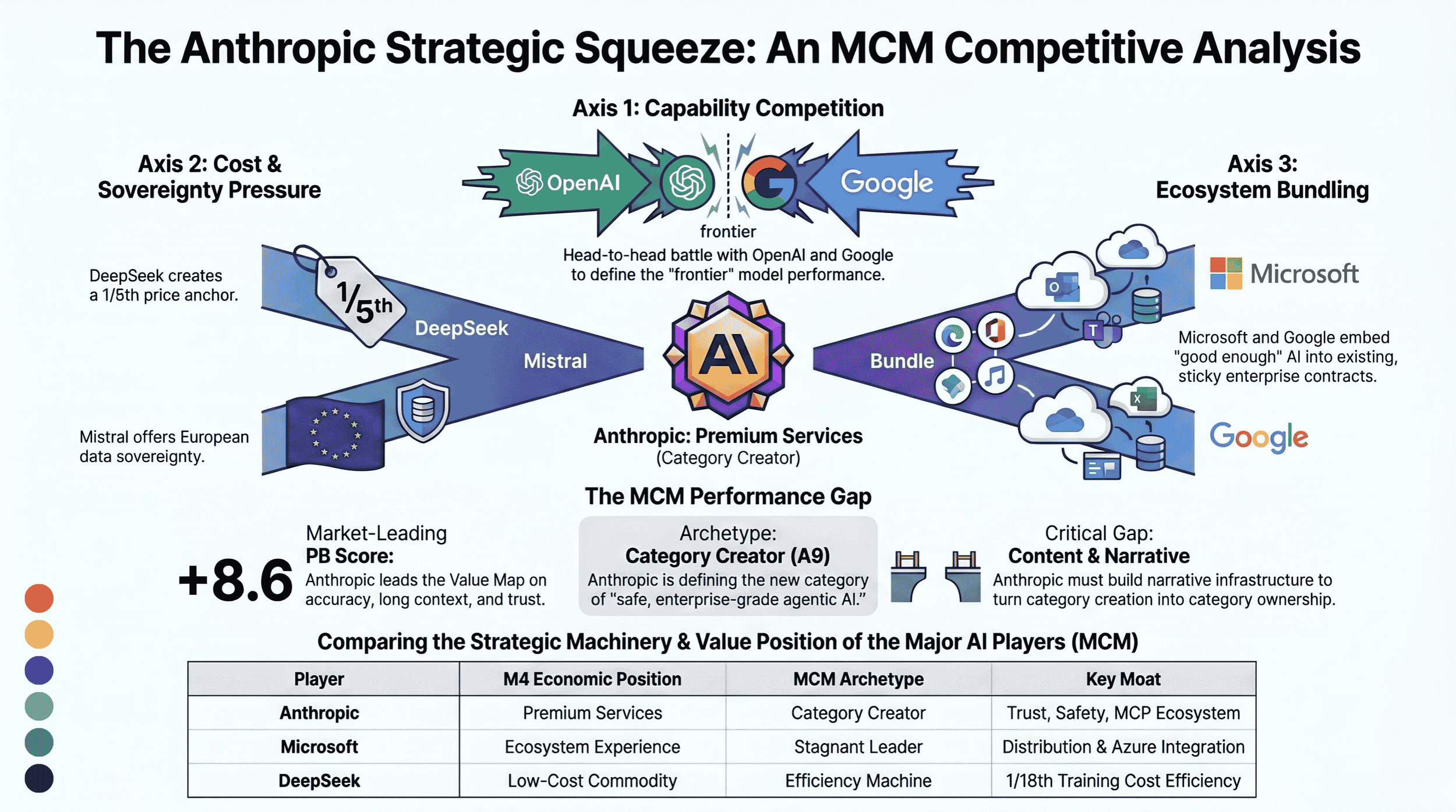

The competitive landscape, when subjected to MCM, reveals not two strategic groups but three competitive axes that pressure Anthropic from different directions simultaneously. The original two-group framing — Western frontier labs vs. efficiency/open-source challengers — was incomplete. The v1.1 analysis adds a third axis: ecosystem incumbents(Microsoft) who compete not on model capability or price, but on distribution, procurement friction, and budget predictability.

MCM Competitive Positioning — Enterprise AI v1.1

M8 × M9 with three competitive axes — Lead Segment: Enterprise Engineering Teams

M9 Value Map — Score per Key Benefit (−3 to +3)M3 × M4 × Revenue Leverv1.1M4 positions, four archetypes, three competitive axes. Microsoft is the most consequential indirect competitor — Copilot holds 42% paid share at 90% of Fortune 100 despite lower quality (SWE-bench: 56.8% vs 80.8%). The gap between product leadership and adoption leadership is filled by content and distribution infrastructure — the same gap MCM identified as below threshold at 520 Content & Stories.

2. M4 Economic Value Mapping: Where Each Player Sits

What This Reveals

The six players occupy four distinct M4 positions, not two:

Commodity layer (DeepSeek): Competes on cost efficiency and accessibility. The value proposition is "comparable performance at a fraction of the price."

Product/Service layer (Mistral): Competes on customisability and sovereignty. The value proposition is "AI you control, on infrastructure you own, in a jurisdiction you trust."

Service layer (Anthropic, OpenAI): Competes on capability, reliability, ecosystem, and trust. Anthropic differentiates on trust and safety; OpenAI differentiates on consumer scale and ecosystem breadth.

Experience/Ecosystem layer (Microsoft, Google): Competes on distribution and integration. The value proposition is not "the best AI" but "AI already embedded in the tools you use." Microsoft and Google do not need to win the AI model race — they need AI to be good enough that enterprises never leave their existing platform relationships.

The critical structural observation: Microsoft and Google occupy the highest M4 position (Experience), which means they compete on a dimension that service-layer players like Anthropic cannot match through product quality alone. You do not out-innovate an ecosystem — you build a different ecosystem.

3. Archetype Analysis: What Game Is Each Player Playing?

What This Reveals

The competitive landscape maps to three archetype families, not two:

Category Creators (Anthropic, OpenAI): Building new categories from scratch. Anthropic is creating "trusted enterprise AI infrastructure"; OpenAI is creating "AI-as-daily-companion." Different categories, same strategic machinery.

Ecosystem Defenders (Microsoft, Google): Protecting existing platform dominance by absorbing AI as a feature layer. Neither Microsoft nor Google needs to build the best AI — they need AI to be good enough that enterprises never leave their ecosystem. The threat to Anthropic: if Copilot becomes "good enough" for 80% of coding tasks, the remaining 20% may not justify a second vendor relationship.

Efficiency Disruptors (DeepSeek, Mistral): Attacking the service layer's premium from below. DeepSeek attacks on cost; Mistral attacks on sovereignty and customisation. Neither can define the category, but both can erode the premium that sustains the Category Creator's economics.

4. The Value Map (M9): Head-to-Head on Key Benefits

What This Reveals

For the enterprise engineering lead segment, the Value Map shows four distinct competitive clusters:

Capability leader (Anthropic): Highest PB score (8.6), driven by code accuracy (+3), long context (+3), privacy (+3), and trust (+3). Wins on the dimensions that matter most for high-stakes enterprise AI work.

Operational leaders (Microsoft, Mistral): Both score 7.4 PB but on different benefit combinations. Microsoft leads on speed (+3), compliance (+3), and pricing transparency (+3) — operational factors that win procurement decisions. Mistral leads on privacy (+3) and pricing (+2) — trust factors with a sovereignty overlay. Microsoft competes for "the enterprise that values predictability." Mistral competes for "the enterprise that values sovereignty."

Scale leader (Google): Moderate PB score (6.3), driven by speed (+3) and compliance (+3). Google's competitive advantage is distribution, not benefit leadership — it reaches more users than any competitor through existing product integration.

Consumer leader / Cost leader (OpenAI, DeepSeek): OpenAI at 5.7 lacks a leading dimension for this segment. DeepSeek at 0.0 leads only on pricing (+3) while trailing catastrophically on trust, privacy, and security. Both are weaker competitors for enterprise engineering teams specifically.

The critical insight: Anthropic and Microsoft both score in the top tier but lead on entirely different benefit clusters. Anthropic leads on capability (what the AI can do). Microsoft leads on operations (how predictable and safe the procurement is). This confirms the L1 v1.1 M6 classification: they are indirect competitors whose benefit profiles are complementary. The enterprise buyer needs both — and 70% of senior engineers use 2–4 AI coding tools simultaneously. But the company that controls the content, narrative, and ecosystem when these tools converge will own the relationship.

5. The Perceived Price vs. Perceived Benefits Map

This is the M8 × M9 positioning map — the core competitive visualisation of MCM Step 1.

Reading the map through MCM's lens:

Anthropic occupies the premium-value quadrant (highest benefits, high price). The Category Creator's natural position.

Microsoft occupies the high-value, moderate-price quadrant (strong benefits, predictable pricing). The Ecosystem Defender's natural position: good enough AI at a price that never surprises the CFO, bundled into contracts the enterprise already has. Microsoft's position on this map is the most dangerous for Anthropic — it sits close to Anthropic on benefits while being dramatically more accessible on price. The only reason it is not directly above Anthropic is the long-context and code-accuracy gap.

Mistral occupies the value-for-money quadrant (solid benefits, lower price, sovereignty premium). Threatens Anthropic's European flank.

Google occupies the high-value, moderate-price quadrant — similar to Microsoft but with less coding-specific strength. Competes on distribution, not on the developer seat.

OpenAI occupies the mid-value quadrant for the enterprise segment. Consumer strength does not translate to enterprise benefit leadership for this lead segment.

DeepSeek occupies the commodity quadrant. Competes for cost-sensitive periphery, not enterprise engineering teams.

6. Strategic Implications: What MCM Tells Anthropic

6.1. The competitive structure is three axes, not two groups

The original two-group framing (frontier labs vs. efficiency challengers) missed the most important competitive axis: ecosystem incumbents. The three axes are:

Axis 1 — Capability competition (vs. OpenAI, Google): Who builds the best model? Anthropic currently leads. This axis is familiar and well-understood.

Axis 2 — Cost/sovereignty competition (vs. DeepSeek, Mistral): Can the premium be justified? DeepSeek pressures on price; Mistral pressures on sovereignty. This axis is structural but manageable.

Axis 3 — Ecosystem/distribution competition (vs. Microsoft): Who owns the enterprise developer relationship? This is the axis most commentators miss and the one MCM identifies as most consequential for Anthropic's long-term position. Microsoft does not need to build a better AI — it needs AI to be good enough that enterprises never leave GitHub, VS Code, and Azure. Copilot at 42% paid market share with 90% Fortune 100 deployment is already "good enough" for most enterprises' baseline needs. The question is whether Anthropic can build sufficient content infrastructure, ecosystem lock-in (MCP), and narrative ownership to justify a second vendor relationship on top of the Microsoft stack.

6.2. The Microsoft paradox: competitor, partner, and customer simultaneously

Microsoft is the most complex competitive relationship in the analysis:

Competitor: Copilot competes for developer mindshare, enterprise AI budget, and procurement priority.

Partner: Azure distributes Claude API; Claude Code is available as a third-party agent inside Copilot Pro+ and Enterprise.

Customer: Microsoft's own engineering teams have widely adopted Claude Code internally.

The paradox is that Microsoft validates Anthropic's product superiority (by choosing Claude Code for its own engineers) while simultaneously undermining Anthropic's market position (by making Copilot the enterprise default). This is the Microsoft competitive strategy in miniature: use the best available AI internally while selling "good enough" AI externally, bundled into an ecosystem that is too sticky to leave.

6.3. DeepSeek is a pricing threat, not a positioning threat

DeepSeek's commodity M4 position means it competes on a different dimension. It does not threaten Anthropic's lead segment directly — trust, security, and privacy scores are structurally negative. But DeepSeek's pricing creates a gravitational effect that makes Anthropic's premium more visible, especially when combined with Microsoft's flat-rate pricing benchmark.

6.4. Mistral is the most dangerous direct competitor

Mistral scores +3 on data privacy (matching Anthropic), +2 on enterprise security, +2 on trust, and +2 on transparent pricing. It also offers data sovereignty on European soil — something Anthropic structurally cannot replicate. For Anthropic's European enterprise expansion, Mistral is a direct rival on the same Value Map dimensions with a structural advantage.

6.5. The three-axis squeeze

Anthropic faces pressure from three directions simultaneously:

From below (DeepSeek, open-source): Commoditisation pressure. "Why pay $25/MTok when DeepSeek R2 delivers 90% for $2/MTok?"

From the side (Mistral, sovereign players): Trust-parity with sovereignty. "Why trust an American PBC when I can get comparable trust from a European player on my soil?"

From above (Microsoft, Google): Ecosystem bundling. "Why add a second vendor when Copilot is already in my GitHub contract and good enough for 80% of tasks?"

The response to this three-axis squeeze, through the MCM lens, is to invest in the dimensions that no axis can replicate:

520 Content & Stories (the identified gap): Category narrative ownership. None of the other five players can define the enterprise AI category — DeepSeek and Mistral lack the market position, Microsoft and Google lack the product depth, OpenAI lacks the enterprise credibility. But Anthropic can only own the narrative if it builds the content infrastructure. The Microsoft paradox sharpens this: Copilot holds 29% workplace adoption vs. Claude Code's 18%, despite Claude Code's 46% "most loved" rating vs. Copilot's 9%. The gap between product leadership and adoption leadership is filled by content and distribution infrastructure.

MCP ecosystem (540 Influencers, Growth Driver): The structural counter to Microsoft's ecosystem lock-in. MCP with 97M+ installs is an open standard that Microsoft's closed Copilot architecture does not match. Formalising MCP into a defensible platform creates switching costs that survive model commoditisation and ecosystem bundling.

210 Purpose / 220 Positioning (both +3): The Pentagon standoff, the PBC structure, the LTBT governance — brand assets that Microsoft (pragmatic enterprise vendor), DeepSeek (Chinese hedge fund subsidiary), Mistral (VC-funded startup), OpenAI (transitioning to for-profit), and Google (advertising company) cannot replicate.

310 Features (Fatal Brake, +3): Continuous capability leadership is the prerequisite for everything else. If Claude Code's SWE-bench lead (80.8% vs. Copilot's 56.8%) erodes, the entire premium-service position collapses.

6.6. The convergence warning

The current complementary pattern (Copilot for autocomplete, Claude Code for agentic work) is unstable. Microsoft is investing in Copilot's agentic capabilities. Anthropic is expanding Claude Code's IDE integrations. The layers will converge. The company that owns content, community, and ecosystem when convergence happens will own the enterprise relationship. The company relying on the "different layer" argument will find itself in a head-to-head distribution fight against Microsoft — without the infrastructure to win it.

7. Summary: The MCM Competitive Positioning Matrix

| Dimension | Anthropic (A9) | OpenAI (A9) | Microsoft (A4) | Google (A4) | DeepSeek (A2) | Mistral (A1) |

|---|---|---|---|---|---|---|

| M4 position | Services (premium) | Services → Experience | Experience (ecosystem) | Services (bundled) | Commodity | Products → Services |

| Archetype | Category Creator | Category Creator | Stagnant Leader | Stagnant Leader | Efficiency Machine | Disruptive Newcomer |

| Revenue (ARR) | ~$30–40B | ~$24B | ~$13B (AI only) | Embedded | ~$1.1B | ~$400M–$1B |

| Primary lever | Acquisition (enterprise) | Acquisition (consumer) | Retention (ecosystem) | Retention (ecosystem) | Acquisition (cost) | Acquisition (sovereignty) |

| Moat | Trust + Safety + MCP | Consumer scale + Brand | Distribution + GitHub/VS Code | Distribution + Infrastructure | Cost efficiency + Open-source | Sovereignty + Customisation |

| Vulnerability | Pricing model; content gap; no sovereignty | Enterprise depth; trust deficit | AI quality gap; dependent on OpenAI models | No coding momentum; fragmented execution | Trust/security; geopolitical risk | Scale; model frontier gap |

| Competitive axis | — | Capability (Axis 1) | Ecosystem (Axis 3) | Ecosystem (Axis 3) | Cost (Axis 2) | Sovereignty (Axis 2) |

| Threat to Anthropic | — | Moderate | High (default + budget) | High (bundling) | Low-direct, High-indirect | High in Europe |

8. The One-Sentence MCM Read

Anthropic's competitive position is structurally strong because it occupies the premium-service position with the best trust moat and the best product in the industry — but that position is under three-axis squeeze from commodity pricing below (DeepSeek), trust-parity sovereignty beside (Mistral), and ecosystem bundling above (Microsoft, Google), and the single most important thing Anthropic can do to defend it is the single thing the MCM analysis identified as below threshold: build the content, community, and ecosystem infrastructure that turns category creation into category ownership before the complementary two-layer pattern converges into a head-to-head distribution fight.

Anthropic Strategic Squeeze - Marketing Canvas Method