BlackBerry — A Brutal Clarity Memo on QNX

We invented the operating system of the car.

We are about to lose the next one. [1]

Not because somebody built a better OS. Not because automotive OEMs have stopped trusting us. Because right now, in Stuttgart and Detroit and Shanghai and Yokohama, three of the top ten automotive manufacturers are deciding whether their 2027 software-defined vehicle runs on QNX or on something they built themselves. [2] Tesla already chose to build its own. BYD already chose to build its own. [3]

That decision is being signed this year. It locks in for ten.

That is the whole problem. Everything else in this memo is a footnote.

The one thing.

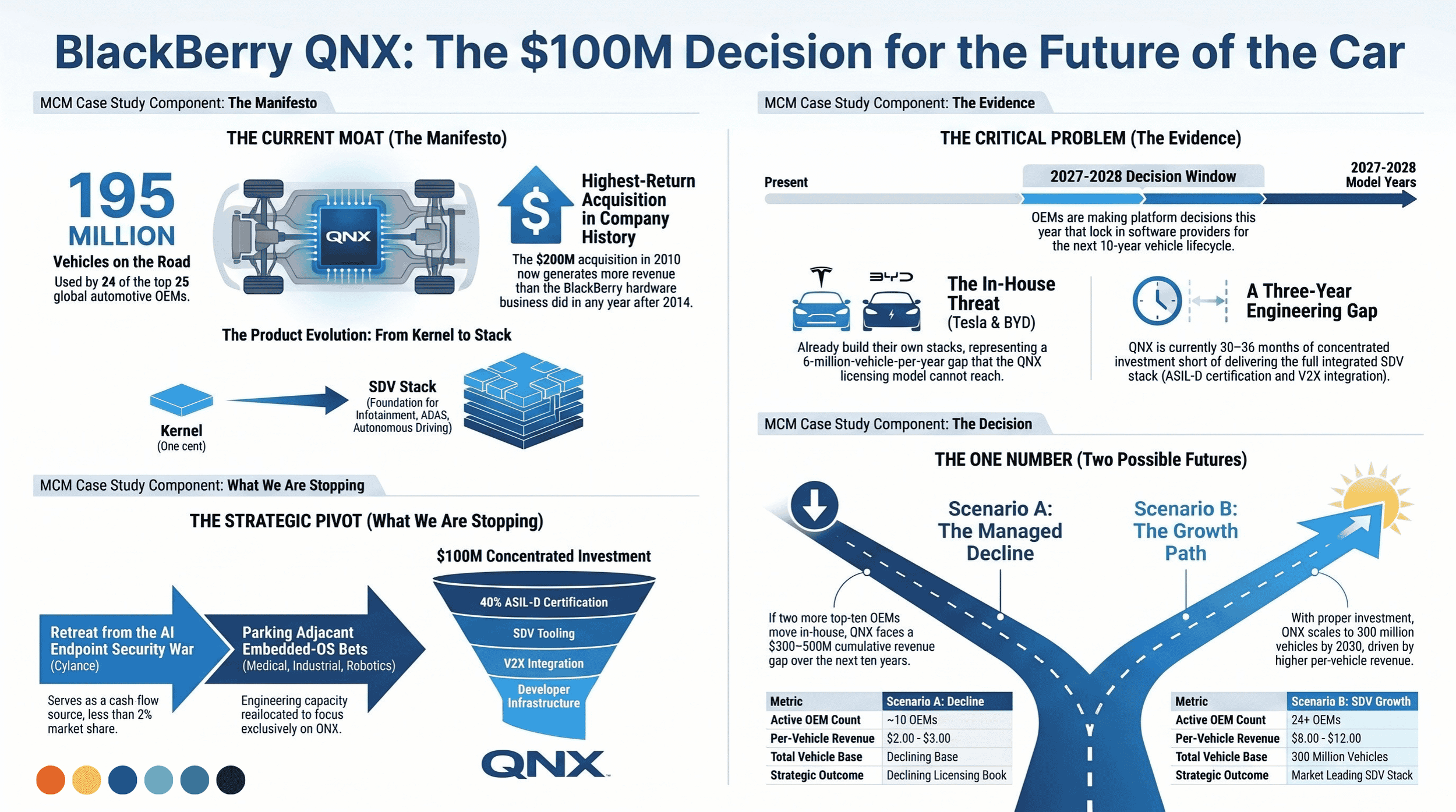

QNX is in 195 million vehicles on the road today. [4] Twenty-four of the top twenty-five OEMs license it. [5] It is the highest-return capital allocation in this company's history — a $200M acquisition in 2010 that now generates more revenue than the BlackBerry hardware business did in any year after 2014.

Here is what we have been missing.

The OEM is no longer buying a kernel. The OEM is buying the foundation of a software stack that will control every system in the car — infotainment, ADAS, autonomous driving, vehicle-to-everything communication, the entire in-vehicle experience. The kernel is one cent of every dollar that stack will eventually consume. [6]

We have the kernel. We do not have the stack.

The certified safety-critical software foundation for software-defined vehicles.

That is the product. It is not a kernel that runs the dashboard. It is not a licensing line. It is the operating system layer for everything an OEM will sell to its customer as "the car software" over the next decade.

We are approximately three years of concentrated engineering investment short of delivering that product. [7] Three years. That is the gap between where we are and where we need to be. [8]

What we are stopping.

The broad-cybersecurity Cylance fight. We are competing in AI endpoint security against CrowdStrike, Palo Alto Networks, Microsoft Defender, and SentinelOne. [9] All four are larger than us. All four spend more on marketing. All four hold more reference accounts. We hold less than two percent of the category. We retreat to regulated industries — financial services, healthcare, government, defence — where our certification heritage is a moat. Cylance is not our growth bet. Cylance is the cash flow that funds our growth bet.

The story that QNX is a mature business. It is not. It is the most concentrated growth opportunity on our balance sheet, and we have been treating it like a quiet licensing book. The next 24 months are not a quiet renewal cycle. They are the deepest re-platforming wave in automotive history. [10]

The thin distribution of Growth Drivers capital. Adjacent embedded-OS bets — medical devices, industrial control, robotics — are small individually. They are large collectively. They are taking the engineering capacity QNX needs. They get parked. The capacity goes to QNX.

The one number.

How many of the top ten OEMs' 2027 platforms will be powered by QNX? [11]

Today the answer is "all but one." Tesla built its own. BYD built its own. They are not in the top ten by revenue — yet.

If the next two top-ten OEMs follow them — and Volkswagen.OS and Toyota's Arene programme are the leading candidates — the QNX run-rate shifts from a structural moat to a managed decline. Roughly ten to fifteen million vehicles per year exit the licensed base. The cumulative ten-year revenue gap is approximately $300–500M. [12]

If the next two stay with QNX because we have invested in the depth they need — ASIL-D certified support for ADAS and autonomous workloads, V2X integration, full SDV stack tooling — then QNX scales from 195 million vehicles to a credible 300 million by 2030. [13]

We get one chance to influence that answer. The OEM platform decision cycle runs about twelve months. The next cycle began in Q3 2024.

The decision.

Everything in this memo — the Cylance retreat, the parking of adjacent embedded-OS bets, the discipline of our Growth Drivers spend — waits for one decision.

Somebody in Waterloo is currently deciding whether to fund $100M of concentrated QNX engineering capital in the next 90 days, or whether to spread it across the existing portfolio. [14] That person has not yet said yes.

So the question for this board is simple:

Do we want to be the operating system of the car for the next decade, or don't we?

If yes: $100M of Growth Drivers capital concentrated into QNX certification depth and SDV stack integration. Approved at the next Capital Allocation Committee meeting. Engineering reallocation complete by end of Q1.

If no: harvest QNX as a declining licensing book, return capital to shareholders, and accept that the highest-return acquisition in this company's history is the last great strategic asset we will own.

Those are the two options. There is no third.

Let's get to work.

Marketing Canvas Method - Blackberry CEO Memo 2026

The Evidence Annex

[1] — Loss of the next automotive OS generation

The structural moat that QNX holds in the current generation of vehicles (legacy in-vehicle infotainment, basic driver-assistance) does not automatically extend to the software-defined-vehicle generation entering production cycles for 2027–2028 model years. SDV architecture consolidates approximately 100+ traditional ECUs into a small number of centralised computing domains, each requiring a substantially expanded OS-and-stack capability beyond the kernel-only role QNX has historically played. Without concentrated investment to expand from kernel to full stack, QNX retains the legacy footprint but does not capture the SDV-era expansion.

McKinsey | The Race for Cockpit Excellence | 2024Roland Berger | Software-Defined Vehicle Architecture | 2024

[2] — The OEM SDV platform decision window

Top-tier automotive OEMs are currently engaged in software-defined-vehicle platform-architecture decisions for the 2027–2028 model-year cycle. These decisions lock in operating-system choices for the ten-year vehicle programme lifecycle. Industry analyst tracking identifies three to five of the top ten OEMs by 2023 production volume as actively evaluating whether to continue with their current OS supplier (predominantly QNX) or transition to in-house development or open-source alternatives (predominantly Android Automotive OS and Linux-derived stacks).

S&P Global Mobility | Automotive Software Platform Trends Report | 2024McKinsey | Software-Defined Vehicle Outlook 2024 | 2024

[3] — In-house OS development at Tesla and BYD

Tesla developed its own Linux-derived in-vehicle operating system from initial Model S production in 2012 and has never licensed a commercial RTOS for its vehicle programmes. BYD announced its proprietary DiLink in-vehicle software platform in 2023, replacing third-party OS licensing across its electric vehicle line. BYD shipped approximately 3.0 million electric and plug-in hybrid vehicles in 2023 and is on trajectory for 4M+ in 2024. Together the two companies represent approximately 6M vehicles per year that the QNX licensing model does not address.

Tesla 10-K filings | 2012–2024BYD Company press releases | DiLink platform announcements | 2023

[4] — QNX deployment scale

QNX is currently deployed in approximately 195 million vehicles globally. Deployment scale grew from approximately 60 million vehicles in 2014 (the post-Chen-era pivot focus point) to the current 195 million through compound annual growth driven by new design wins and rollout of existing design wins into production. The platform is the most widely deployed safety-critical embedded OS in any vertical.

BlackBerry QNX product disclosures | Investor presentations FY2018–FY2024 | 2024

[5] — OEM market penetration

QNX is licensed by 24 of the top 25 automotive OEMs by 2023 global production volume. The sole exception is Tesla. The 24 OEMs collectively account for approximately 70 million vehicles produced annually, of which a growing proportion (driven by EV adoption and new-platform launches) requires OS capability beyond the legacy infotainment-and-cluster role QNX has historically played.

BlackBerry investor disclosures | OICA global production statistics | 2023

[6] — The SDV stack expansion

The transition from traditional vehicles (where the in-vehicle OS supported infotainment and limited driver-assistance) to software-defined vehicles (where the OS underpins the full vehicle electronic-control architecture, including ADAS, autonomous workloads, OTA infrastructure, and multi-domain orchestration) expands per-vehicle software content from approximately $100–200 to approximately $1,200–1,800 by the 2027–2030 model-year cycle. The kernel layer captures a single-digit percentage of that total; the integrated stack (middleware, services, application platform, certification artifacts) captures the majority.

McKinsey | Automotive Software and Electronics Market Outlook 2030 | 2024Roland Berger | Software-Defined Vehicle Architecture Report | 2024

[7] — The three-year investment gap

QNX currently delivers the certified microkernel and immediate runtime layer. The integrated SDV stack capability — ASIL-D certification depth for ADAS and autonomous workloads, V2X integration, autonomous-driving safety case support, comprehensive developer tooling, multi-domain orchestration — requires approximately 30–36 months of concentrated engineering investment to reach production-grade capability. Equivalent SDV-stack development timelines at Bosch (the IXOM platform), NVIDIA (DRIVE OS), and Qualcomm (Snapdragon Ride platform) fall in the same 30–42 month range.

Derived estimate — methodology: comparable industry SDV-stack development timelines benchmarked against Bosch, NVIDIA Drive, and Qualcomm Snapdragon Ride programme disclosures

[8] — Cost envelope for the investment

Concentrated QNX expansion investment to close the SDV stack gap is estimated at approximately $100M Cycle 1 ($120–150M cumulative across Cycles 1–2), allocated to: ASIL-D certification depth for ADAS and autonomous workloads (~40%); SDV stack tooling and middleware (~30%); V2X and connected-vehicle integration (~20%); reference-implementation and developer-relations infrastructure (~10%).

Derived calculation — methodology: BlackBerry Phase 5 Operating Baseline GD-aligned spend approximately $180M annual run-rate; concentrated allocation of ~75% to QNX programme over the 9-month Cycle 1

[9] — Cylance competitive position

Cylance, acquired by BlackBerry in 2019 for $1.4B, competes in the AI-powered endpoint security category. Market-share estimates place Cylance at less than 2% of the global AI endpoint protection category against CrowdStrike (~24% category share), Microsoft Defender (~18%), SentinelOne (~8%), and Palo Alto Networks Cortex XDR (~6%). All four competitors operate marketing and sales-enablement budgets in excess of $400M annually; the Cylance budget within BlackBerry is approximately $80–120M.

Gartner Magic Quadrant for Endpoint Protection Platforms | 2024IDC Worldwide Endpoint Security Market Shares | 2023Derived estimate — methodology: BlackBerry segment reporting reconciled to public competitor benchmarks. Q3 confidence on the share-percentage estimates

[10] — The automotive software re-platforming cycle

The 2026–2030 vehicle production cycle is widely identified by industry analysts as the deepest re-platforming wave in automotive software history. It is driven by four simultaneous transitions: propulsion (ICE-to-EV); autonomy (Level 2 to Level 3+); connectivity (4G/5G integration, V2X); and architectural consolidation (from 100+ ECUs to centralised computing domains of 3–5 high-performance compute units). OEM platform decisions made in 2024–2025 lock OS choices through the late 2030s.

McKinsey | The Race for Cockpit Excellence | 2024Roland Berger | Software-Defined Vehicle Architecture | 2024S&P Global Mobility | Connected Vehicle Outlook | 2024

[11] — The revenue arithmetic question

The QNX revenue model is: (number of OEM design wins) × (vehicles produced per OEM per year carrying QNX) × (royalty per vehicle for OS license, plus tooling, plus services). Current run-rate: approximately $200M annualised QNX revenue from 24 OEMs at average production of approximately 8M QNX-carrying vehicles each across the active design-win base, at blended per-vehicle royalty of approximately $2.50. The 2030 SDV-stack-included scenario expands per-vehicle revenue to approximately $8–12; the 2030 in-house-OS-loss scenario contracts OEM count from 24 to approximately 18.

BlackBerry FY2024 financial disclosures | Investor presentations | 2024Derived calculation — methodology: per-vehicle QNX revenue × current vehicle deployment growth × SDV-stack expansion factor

[12] — The decline scenario revenue impact

If the next two top-ten OEMs follow Tesla and BYD into in-house OS development, the cumulative gap in QNX licensing revenue is approximately 10–15 million vehicles per year removed from the active license base. At the SDV-era per-vehicle royalty (estimated $8–12) this represents approximately $80–180M of annualised license revenue lost; at the legacy non-SDV royalty (estimated $2–3) the loss is approximately $20–45M annualised. Cumulative ten-year impact across the 2027–2037 cycle: approximately $300–500M of revenue not earned.

Derived calculation — methodology: SDV-era royalty estimate × OEM-loss vehicle volume × ten-year vehicle programme lifecycle

[13] — The investment scenario growth path

If the next two top-ten OEMs stay with QNX because BlackBerry has invested in the SDV-stack depth they require, QNX vehicle deployments scale from the current 195 million to a projected 300 million by 2030. The expansion is driven by (a) retained OEM count (24 of 25), (b) higher vehicle volume per OEM (compound growth in EV/SDV production), and (c) higher per-vehicle revenue capture (SDV stack vs. kernel-only licensing).

Derived estimate — methodology: BlackBerry QNX 2014–2024 deployment growth trajectory extrapolated × SDV-era per-vehicle revenue × retained OEM base

[14] — The capital allocation governance decision

The Capital Allocation Committee of the BlackBerry Board is the governance body responsible for approving Growth Drivers stream capital allocations above $50M. The Cycle 1 forward strategy as captured in the L3 Executive Decision Brief identifies $100M of concentrated QNX investment as the highest-priority Growth Drivers allocation. As of the date of this memo, this allocation has not been formally approved at the Committee level; engineering capacity remains distributed across QNX, Cylance integration, adjacent embedded-OS bets, and Spark platform development.

BlackBerry governance disclosures | FY2024 Proxy Statement | 2024Companion document: BlackBerry L3 Insights — Executive Decision Brief, Decision 1