BlackBerry — A Strategic History Memo, 1999–2024

The arc in one paragraph

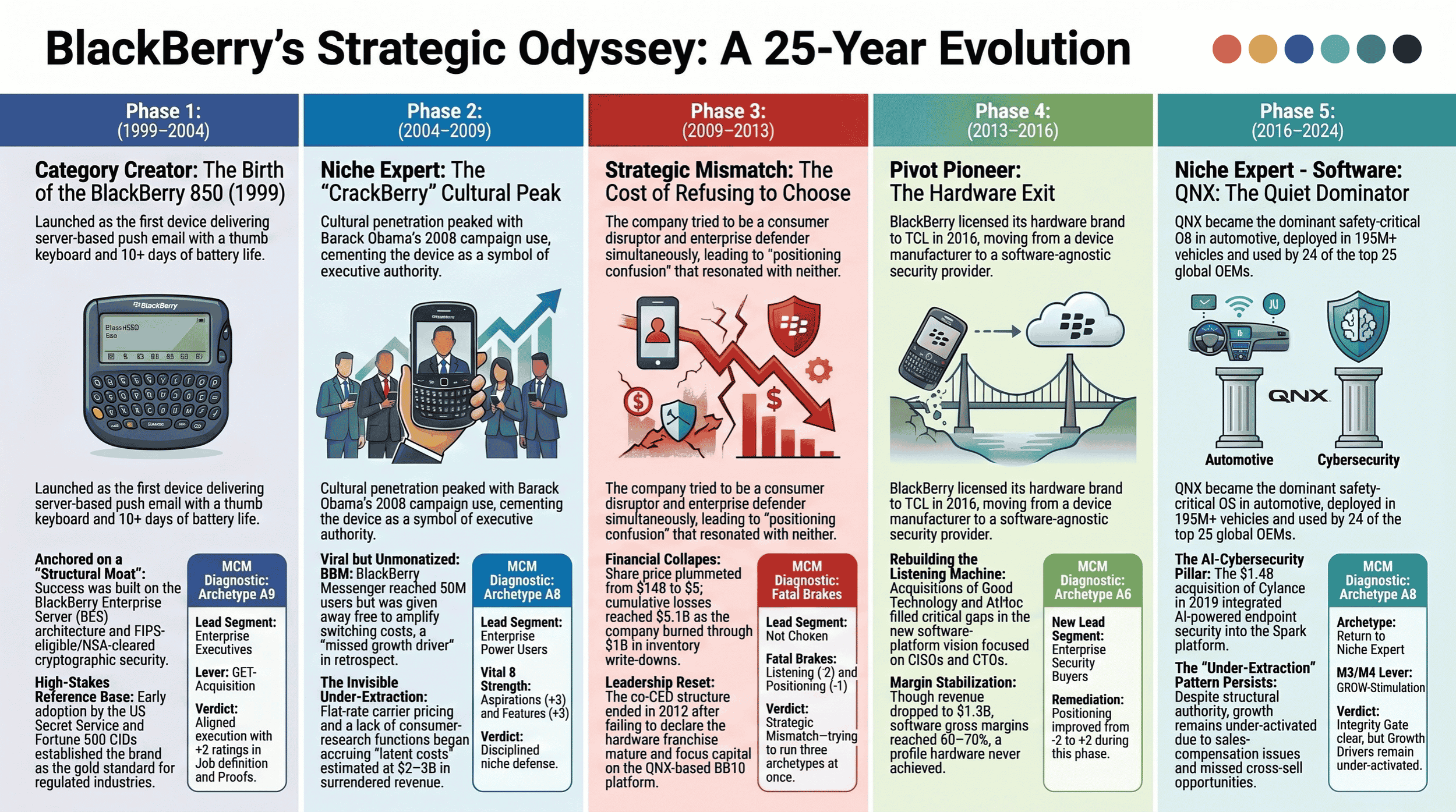

BlackBerry's strategic history across twenty-five years is one of the cleanest multi-decade archetype trajectories in modern technology business: a Category Creator (1999–2004) that named the job of secure mobile email before the market did; a Niche Expert (2004–2009) that built a structural moat in enterprise mobile productivity and reached $19.9B in revenue with 85 million subscribers at peak; a four-year Strategic Mismatch (2009–2013) in which the company tried to be a consumer disruptor and an enterprise defender simultaneously, refused to harvest its hardware franchise, and burned $5.1B in cumulative losses while watching its share price fall from $148 to approximately $6; a Pivot Pioneer (2013–2016) under John Chen that executed the most credible late-stage rescue in the history of mobile devices; and a recovered Niche Expert (2016–2024) operating today as a $700M software business with structural authority in two niches — safety-critical automotive operating systems and enterprise cybersecurity for regulated industries. The case is interesting not because it ends well or badly but because all five phases happen to the same company and the inflection points are visible in real time.

Marketing Canvas Method - Blackberry Historical Case Study

Phase 1 — Category Creator | 1999–2004

Characterisation: The company invents a category that does not yet exist.

Research In Motion launched the BlackBerry 850 in January 1999 as the first device to deliver server-based push email to a portable form factor with a thumb keyboard. The company was Canadian, small (~600 employees), and led by a technical co-CEO (Mike Lazaridis, who designed the radio architecture) and a commercial co-CEO (Jim Balsillie, who managed carrier negotiations and enterprise sales). The first commercial wins were in the segments that needed exactly this product and would pay any price for it: the US Secret Service deployed BlackBerry in 2000; the US State Department followed; Goldman Sachs and other financial-services firms moved next; Fortune 500 CIOs in regulated industries became the early reference base.

The product was anchored on three structurally defensible capabilities. BES — the BlackBerry Enterprise Server — was a server-side push architecture that no competitor had matched, and the radio-efficiency advantage it produced (10+ days of standby battery life against the 1–2 days that early competitors offered) was real. The QWERTY keyboard was purpose-designed for thumb typing in landscape orientation, and the industrial form was instantly recognisable. The cryptographic implementation was FIPS-eligible and NSA-cleared, which made BlackBerry the only credible choice for any government or financial-services buyer with serious security requirements.

The brand naming exercise — Lexicon Branding produced "BlackBerry" in 1999 — was a fortuitous choice that became one of the most durable brand assets in technology. The device became a verb. The company crossed one million enterprise subscribers in FY2004 with revenue of approximately $595M. Carrier relationships in North America were locked; UK and European expansion began in 2002.

The phase's signature: category creation executed with discipline. The job was defined precisely (secure push email for the office-constrained executive); the moat was built (BES + radio + certification); the brand was named; the reference base was established.

MCM diagnostic support:

Category Creator

| Lead Segment | Enterprise executive and government official — information-dependent, office-constrained C-suite professionals |

|---|---|

| Customer type | Underserved Switcher (previously: pager + laptop combination with no integration) |

| M3 / M4 / Lever | Introduction / Services / GET-Acquisition |

| Archetype | Category Creator A9 — uncontroversial matrix-default selection |

| Vital 8 strengths | Job definition; Features; Proofs; Listening; Influencers — all at +2 |

| Mechanism issues | None active. One forward-looking row flagging the absence of a content-marketing function for the maturing category — invisible cost in Phase 1; material cost in Phase 3 |

| Verdict | Aligned execution across all streams |

Phase 2 — Niche Expert | 2004–2009

Characterisation: The company defends and deepens a niche it now owns; cultural penetration peaks; one structural mistake is set in motion.

The category formed. Competitors entered (Good Technology, Microsoft Windows Mobile, Palm Treo, Nokia E-series) but none could replicate the BES architecture or the certification estate. BlackBerry's response was to deepen the niche rather than to scale operationally. The product line expanded — Pearl in 2006, Curve in 2007, Bold in 2008 — each iteration sharper on the QWERTY ergonomics, battery life, and BES integration that defined the category. Carrier partnerships expanded to over 100 countries. International revenue grew from less than 10% of total in 2004 to approximately 40% by 2009.

BBM — BlackBerry Messenger — launched in 2005 as a free instant-messaging service for BlackBerry-to-BlackBerry users. It became the company's most viral product, reaching 50 million users at peak. It was never monetised. The decision to give BBM away free was made on the assumption that it served as a switching-cost amplifier for the underlying device platform; the assumption was correct but commercially incomplete.

The cultural penetration was the period's most visible signature. The "CrackBerry" nickname emerged in executive circles in 2002–2004 and became mainstream cultural shorthand by 2006. Barack Obama was photographed with a BlackBerry during his 2008 presidential campaign and continued to use one in office in January 2009 — a cultural moment that consolidated BlackBerry as the device of senior executive and political authority. Revenue reached $11B in FY2009; the subscriber base reached 32 million and was growing.

Beneath the strong execution, two latent strategic costs were accruing. The BIS (BlackBerry Internet Service) flat-rate pricing structure, designed for carrier-billing simplicity, capped average revenue per user at a level well below what the segment composition could have supported. And the company built no consumer-research function — none of significant scale, none with operating headcount in proportion to engineering — because the enterprise listening machine that drove product decisions in Phase 1 still worked for enterprise buyers. Both costs were invisible during Phase 2. Both became existential in Phase 3.

The phase's signature: disciplined niche defence with very high cultural relevance, and a slow under-extraction of the installed base whose cumulative cost across the phase was an estimated $2–3B in surrendered ARPU.

MCM diagnostic support:

Niche Expert

| Lead Segment | Enterprise power user — primarily financial services, legal, consulting, government |

|---|---|

| Customer type | Under-Optimized Power User (subscribers paying BIS/BES fees but using a fraction of available features) |

| M3 / M4 / Lever | Growth / Products / KEEP-Retention |

| Archetype | Niche Expert A8 — defensible deviation from matrix-default Efficiency Machine A2, justified by the structural-moat criterion |

| Vital 8 strengths | Features at +3 (above-target); Proofs at +3; Aspirations at +2/+3 (Obama peak); Job, Positioning, Prices, Influencers all at +2 |

| Mechanism issues | ARPU below GD-target (BIS flat-rate pricing); BBM unmonetised; no consumer-listening infrastructure built (latent) |

| Verdict | Strong execution; two missed Growth Drivers (ARPU lift, BBM monetisation); one latent capability gap (consumer voice-of-customer) |

Phase 3 — Strategic Mismatch | 2009–2013

Characterisation: The company refuses to choose between two segments and pays the cost of indecision in real time.

The disruption signal was visible by 2007. Apple launched the iPhone in January 2007 and the App Store followed in July 2008. Android arrived in late 2008. Lazaridis's public assessment — that the iPhone's browser-based architecture "will kill the network" — was the canonical moment of dismissal: the M10 High Disruption signal was filed rather than acted on. By 2009 the consumer smartphone market was doubling annually; by 2010 enterprise IT departments were starting to allow iOS devices on managed networks; by 2011 carrier retail floors had pivoted from BlackBerry-led displays to iPhone-led displays in every major market.

BlackBerry's response was to attempt three archetypes simultaneously. The company launched consumer-targeted devices — Storm in 2008, Torch in 2010, Storm 2 in 2009 — in an attempt to compete with iPhone on touchscreen experience. The first Storm was critically panned ("software side is unpolished, confusing and not ready for primetime"). The company also maintained its enterprise hardware refresh cycle — Bold 9900 in 2011, still selling five million units in 2012 — treating it as a growth franchise. And it began the platform pivot to a new operating system, acquiring QNX in April 2010 for $200M with the intention of using it as the foundation for a next-generation BlackBerry device. The 2011 advertising tagline became "for business AND personal" — an attempt to span both segments that resonated with neither.

The PlayBook tablet launched in April 2011 without native email, calendar, or contacts applications — a discovery that consumer reviewers and buyers regarded as a dealbreaker. The product was eventually written down by ~$485M; cumulative inventory and development losses exceeded $1B. Internally, the discovery surfaced something the company had not known: it had no consumer-research function capable of telling the product team that a consumer buying a BlackBerry tablet would expect BlackBerry email. The consumer-research headcount across the entire organisation was under 20 against more than 5,000 in engineering.

The co-CEO governance structure (Lazaridis owned the technical platform; Balsillie owned the carrier and sales relationships) made the alternative impossible. The structural strategic move available in 2010 — ring-fence the enterprise hardware business as a Value Harvester to generate cash, concentrate the pivot capital on one platform (the QNX-based BB10), and accept that the company was operating two business units with separate Lead Segments — required a single executive willing to declare the enterprise hardware franchise mature. Neither co-CEO could make that declaration while the other was committed to its growth. Both resigned in January 2012, replaced briefly by Thorsten Heins.

Revenue peaked at $19.9B in FY2011 with 85 million subscribers and then collapsed. Revenue fell to $11B in FY2013. The share price fell from $148 (June 2008) to approximately $6 (mid-2013). Cumulative losses 2012–2014 reached $5.1B. BB10 launched in January 2013 — three years after the QNX acquisition and well after the consumer smartphone market had consolidated around iOS and Android. The Z10 flagship sold approximately one million units in its launch quarter against an estimated ten-million unit break-even.

The phase's signature: the cost of refusing to make a Step 0 strategic decision. The four-year sequence is the most extensively documented example in mobile-industry history of what happens when a company operates without a chosen Lead Segment in a disrupted market.

MCM diagnostic support:

Strategic Mismatch

| Lead Segment | Not chosen — the Step 0 fault that propagates through every downstream dimension |

|---|---|

| M10 Disruption | High — override to Pivot Pioneer A5 was available 2009–2010; not invoked |

| Archetypes attempted | Disruptive Newcomer A1 for consumer + Stagnant Leader A4 for enterprise hardware + Pivot Pioneer A5 for BB10 platform — simultaneously |

| Archetype refused | Value Harvester A6 for enterprise hardware — the missing piece that would have funded the A5 pivot at the right scale |

| Fatal Brakes below 0 | Positioning (−1); Listening (−2, the deepest in the case) |

| Mechanism cluster | Four of five below-threshold mechanisms (Positioning, Listening, Job, Proofs) trace to a single Step 0 fault — the central analytical finding the v5.0 method's mechanism discipline surfaces |

| Cost of inaction | Approximately $6B cumulative, three years of pivot delay, share price collapse $148 → ~$6 |

| Verdict | Strategic Mismatch — A1+A4+A5 attempted without commitment; A6 refused as a matter of organisational identity |

Phase 4 — Pivot Pioneer | 2013–2016

Characterisation: A late-stage rescue executes the strategic moves the previous leadership refused.

John Chen joined as CEO in November 2013, with $2.6B in cash and burn rate approaching $1B per year — a runway of 24 to 30 months without revenue stabilisation. His first 90 days produced the strategic moves that defined the period. In February 2014 he gave the public commitment that broke the company's hardware identity: "If you bring an iPhone to work, we'll manage it." The statement positioned BlackBerry as a device-agnostic enterprise security software provider — a pivot from "the secure phone" to "the security platform for every phone."

BES 12 launched later in 2014 as the first genuinely cross-platform unified endpoint management product, supporting iOS, Android, and Windows devices alongside BlackBerry. The BlackBerry Security Summit launched the same year, beginning the slow rebuild of CISO-segment listening infrastructure that the company had never possessed. Workforce reductions cut headcount from ~17,500 at FY2011 peak to ~7,000 by FY2016. The hardware exit decision, which the v5.0 analysis identifies as having been correct in 2010, was finally made in October 2016 when BlackBerry licensed the BlackBerry-branded hardware business to TCL of China — three years late but executed cleanly when it came.

The acquisition engine became the primary growth mechanism for software-platform expansion. Good Technology was acquired for $425M in September 2015, adding a competing enterprise mobility management product, an installed base of approximately 6,200 customers, and a software-trained sales force. AtHoc (emergency mass communications) followed in 2015. Encription (cybersecurity consulting) followed in 2016. Each acquisition addressed a specific gap in the software-platform vision Chen had committed to publicly.

The financial result was not yet recovery but stabilisation. Revenue settled at approximately $1.3B in FY2017 — well below FY2014 levels but with software gross margin profiles in the 60–70% range that hardware revenue had never delivered. The cash position stabilised at ~$1.7B. The company was no longer in existential danger.

The phase's signature: an A5 Pivot Pioneer executing the strategic moves the previous leadership had refused, with three-year-late timing on the hardware exit that cost approximately $1.5–2B in unnecessary hardware-programme spend.

MCM diagnostic support:

Pivot Pioneer

| Retiring Lead Segment | Enterprise BlackBerry device user (the professional for whom the physical keyboard and BBM were the buying reason) |

|---|---|

| New Lead Segment | Enterprise security buyer — CISO/CTO of regulated-industry organisation |

| M3 / M4 / Lever | Decline (hardware) + Growth (software) / Services / Pivot |

| Archetype | Pivot Pioneer A5 — M10 High Disruption override invoked; survival requirement, not discretionary |

| Fatal Brakes at entry | Positioning (−2) and Listening (−1) — both blocked Integrity Gate at Chen's arrival |

| Step 4 outcomes | Positioning declaration: Aligned (cleanest Fatal Brake remediation in the case, −2 → +2 across the phase); CISO listening: Partial (~2 years to robust capability); Hardware harvest: Aligned-but-late (Oct 2016, 3 years overdue); Acquisition engine: Aligned (Good Technology, AtHoc, Encription); Cross-platform BES 12: Aligned |

| Verdict | Correct A5 pivot direction; three-year delay in the A6 hardware harvest is the period's principal execution drag |

Phase 5 — Niche Expert (Software) | 2016–2024

Characterisation: The company stabilises as a software-platform Niche Expert with structural authority in two distinct niches; the recovered position is durable but not yet fully extended.

By 2016 BlackBerry was no longer a hardware company. The TCL licensing arrangement removed hardware from the income statement; the remaining business was structured around two software platforms. The first was the cybersecurity platform — BlackBerry UEM (the former BES rebranded), Cylance (acquired in January 2019 for $1.4B), AtHoc, and the broader Spark unified platform that integrated them. The second was QNX — the embedded operating system that had originally been acquired in 2010 to power consumer phones and had instead become the dominant safety-critical operating system in the global automotive industry.

The Cylance acquisition was the period's largest single capital allocation. At closing it brought AI-powered endpoint security technology, approximately 4,000 enterprise customers including reference accounts in financial services and government, and a brand position in the emerging AI-cybersecurity category. The integration into Spark took longer and produced more friction than expected; competitive positioning against larger AI endpoint vendors (CrowdStrike, Microsoft Defender, SentinelOne, Palo Alto Cortex) proved structurally difficult.

QNX, by contrast, scaled quietly into the most consequential strategic asset in the company's portfolio. By 2022 QNX was deployed in over 195 million vehicles globally and licensed by 24 of the top 25 automotive OEMs. The platform's ISO 26262 ASIL-D certification estate represented a moat that competitors could not replicate without multi-year, multi-hundred-million-dollar investments. Annual QNX revenue reached approximately $200M with structurally rising per-vehicle royalty as software-defined vehicle architectures expanded the OS layer's scope.

Total company revenue stabilised at approximately $700–720M in FY2022 with consolidated software gross margins in the 70–75% range. John Chen retired in November 2023; John Giamatteo (former Cylance CEO) succeeded him with a stated agenda of segment focus — separating the IoT segment (QNX) and the Cybersecurity segment (Spark + Cylance) into more clearly delineated reporting and operational structures.

The forward strategic agenda inherits one twenty-year structural pattern that has not yet been resolved: the same family of mechanisms that left ARPU under-extracted in Phase 2 (BIS flat-rate pricing), Phase 3 (unmonetised BBM), and Phase 4 (acquisition-driven new-logo focus) now appears in Phase 5 as Spark cross-sell motion that has not been engineered into the sales-compensation structure. The recovered Niche Expert has cleared its Integrity Gate but has not yet activated its Growth Drivers.

The phase's signature: the canonical multi-decade A-trajectory has completed — Category Creator to Niche Expert to Strategic Mismatch to Pivot Pioneer to Niche Expert — and the recovered Niche Expert is now operating with the same structural posture as Phase 2 but pointed at a fundamentally different set of niches.

MCM diagnostic support:

Niche Expert (Software)

| Lead Segment | Enterprise security authority buyer — CISO/CTO of regulated-industry or safety-critical organisation |

|---|---|

| Customer type | Under-Optimized Power User (within installed BES base, ARPU expansion via cross-sell) + Underserved Switcher (in automotive safety-critical OS) |

| M3 / M4 / Lever | Maturity (cybersecurity) + Growth (automotive OS) / Services / GROW-Stimulation |

| Archetype | Niche Expert A8 — return to the same archetype as Phase 2; new niches |

| Vital 8 at target | Features, Positioning, Proofs, Job, Prices — all at +2 |

| Below target | ARPU (+1, the 20-year cross-phase pattern); Influencers (+1); Aspirations (+1) |

| Forward strategic agenda | Five decisions framed in the L3 Executive Decision Brief: QNX automotive concentration; Cylance sub-niche sharpening; ARPU cross-sell motion fix; Influencer cadence rebuild; Aspirations re-engineering |

| Verdict | Recovered A8 with structural authority in two niches; Integrity Gate clear; Growth Drivers under-activated |

ElementReadingLead SegmentEnterprise security authority buyer — CISO/CTO of regulated-industry or safety-critical organisationCustomer typeUnder-Optimized Power User (within installed BES base, ARPU expansion via cross-sell) + Underserved Switcher (in automotive safety-critical OS)M3 / M4 / LeverMaturity (cybersecurity) + Growth (automotive OS) / Services / GROW-StimulationArchetypeNiche Expert (A8) — return to the same archetype as Phase 2; new nichesVital 8 at targetFeatures, Positioning, Proofs, Job, Prices — all at +2Below targetARPU (+1, the 20-year cross-phase pattern); Influencers (+1); Aspirations (+1)Forward strategic agendaFive decisions framed in the L3 Executive Decision Brief: QNX automotive concentration; Cylance sub-niche sharpening; ARPU cross-sell motion fix; Influencer cadence rebuild; Aspirations re-engineeringVerdictRecovered A8 with structural authority in two niches; Integrity Gate clear; Growth Drivers under-activated

Synthesis — what the five phases together teach

Two characteristics persist across all five phases of this company's history and explain both the successes and the failures.

The first is technical authority as a structural moat. BlackBerry has always been a structural-moat company. The BES server architecture in Phase 1, the cryptographic certification estate from Phase 2 onward, the QNX safety-critical operating system in Phases 4 and 5 — each represented genuine technical depth that competitors could not replicate by scaling operational excellence. The company's strategic successes (Phase 1 category creation, Phase 2 niche defence, Phase 5 dual-niche recovery) have all rested on building defensible technical depth in a specific niche. The company's strategic failures (Phase 3 in particular) have rested on diluting that depth across too many parallel programmes for too many segments at once. The QNX acquisition in 2010 — bought for one purpose (the operating system for the next BlackBerry phone) and ultimately serving another (the dominant operating system in cars) — is the highest-return capital allocation in the company's history and is the cleanest demonstration of what concentration on structural moat produces over time.

The second is a persistent under-extraction from the installed base. Across Phases 2, 3, 4, and 5 the same family of mechanisms — under-engineered pricing architectures, unmonetised viral assets, sales-compensation structures that reward new-logo wins over expansion, cross-sell motions that exist on the platform but not in the field — has left revenue per customer below where the segment composition could have supported. This has been a twenty-year pattern. Phase 5's forward strategy is the first phase in which the management team has both the operational discipline and the integrated platform (Spark) to address it. Whether it does is one of the most consequential open questions in the case.

A third observation, more general: the case is structurally interesting because Phase 3 — the four-year Strategic Mismatch — is the period in which the v5.0 MCM framework's distinctive diagnostic discipline is most clearly demonstrated. What looked at the time like five separate marketing and product failures (positioning confusion, brand erosion, product mismatches, listening gaps, pricing pressure) is shown by the mechanism analysis to have been one strategic-decision failure cascading through five dimensions. The Lead Segment that the company refused to choose, and the consumer-segment listening infrastructure it never built, were the single underlying condition. Treated as five failures the response generates five remediation initiatives, distributes capital across them, and produces incremental partial improvements. Treated as one mechanism cluster the response concentrates on the governance decision (commit a Lead Segment, or commit two business units with separate Lead Segments) and on the capability build (a consumer-research function at scale). The five-into-one finding is the v5.0 method's structural contribution to this case, and it is the finding that makes the case instructive rather than merely historical.