Nokia and the iPhone: The Memo Never Written, July 2007

Imagine you are the CEO of Nokia in July 2007. The iPhone has just launched. Apple has sold 270,000 of them in thirty hours. The press is treating it as something different from a phone. Your N95 has more features, more 3G, more megapixels, and more global distribution. The instinct in the building is to build a better N-series. You sit down with the Marketing Canvas Method for one honest afternoon. Here is what you learn. You are not running one phone company; you are running two businesses under one P&L, and they need two different strategies. The high-end smartphone tier is now in a fight Apple has chosen the terms of, and your existing playbook does not work in it. The real weakness is not pricing, and not features — it is positioning at the high-end. The mass-market phone business is still a growth machine and must not be disturbed in the response. The decision is not on the CMO's desk; it is on yours. And you have eighteen months. Probably less. The Brutal Clarity Memo below is what that afternoon produces.

MEMORANDUM

TO: Olli-Pekka Kallasvuo, President & Chief Executive Officer; Nokia Group Executive Board FROM: Office of Strategic Planning DATE: 30 July 2007 RE: The iPhone is not a handset. Separate Multimedia from Mobile Phones before Q4 budget lock.

CLASSIFICATION: Board-restricted. Two pages.

Page 1 — The Manifesto

We are losing the argument we are not in

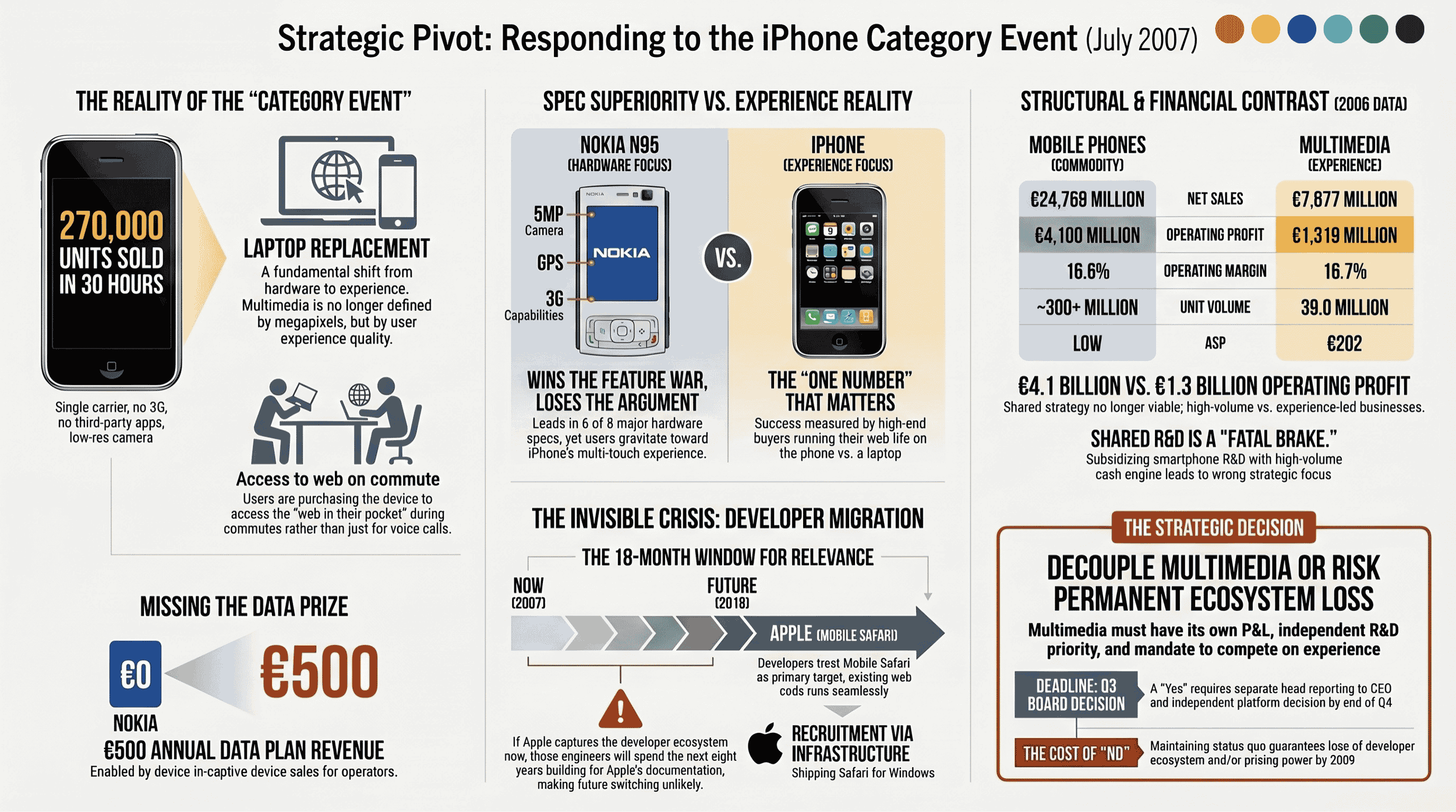

In the first thirty hours on sale Apple activated 270,000 phones at $499 or $599 each, on one US carrier, with no third-party applications, no 3G radio, and a two-megapixel camera. [1] The phone is missing every feature our N95 launched with in March. [2] The press is comparing them anyway. The user is buying anyway.

That is not a competitive event. That is a category event.

A twenty-eight-year-old web developer in San Francisco is not buying the iPhone instead of the N95. He is buying the iPhone instead of his laptop on the train. [3] We do not have a phone in that argument. We are not losing it. We are not in it.

That is the whole problem. Everything else is a footnote.

The One Thing

Our Multimedia segment ships devices at an average sales price of approximately €200. [4] Our customer in the developed-market premium tier pays his operator approximately €40 a month for the data plan that follows the device — €500 a year. [5] We capture none of it. We sold him a phone built to make a call.

The iPhone is a phone built to make him use the data plan. Full HTML web browsing, the iPod inside the phone, visual voicemail negotiated with the carrier, a multi-touch screen engineered around the thumb. [6] Every component pushes him toward the data subscription. Every component of our N-series points the other way.

The Multimedia tier is no longer a hardware tier. It is an experience tier.

The product that matters is the web in his pocket, not the phone in his hand.

We are not behind on megapixels or GPS. We are behind on the only question that matters in that tier, by approximately eighteen months of platform work.

What We Are Stopping

The "N95 is the iPhone-killer" framing. Our communications around the N95 launch and through this quarter have led with a feature comparison against the iPhone. [7] The feature comparison wins. We are answering a question nobody asked while the question that was asked is being answered by Cupertino.

Symbian as the unstated default for everything above €300. Symbian was the correct platform for the €400 converged device of 2003. Whether it is the correct platform for the €600 experience-led device of 2009 is an open question we have not asked. [8] Our 2008 product roadmap will set the answer by default.

One Devices & Services strategy for two structurally different businesses. Mobile Phones earned €4.1 billion operating profit in 2006. Multimedia earned €1.3 billion. [9] They share an R&D allocation, a CEO, and a quarterly review. Mobile Phones is selling a commodity into the largest market expansion in the industry's history. Multimedia is now selling an experience into a market whose definition was rewritten on 29 June.

The Problem We Haven't Named Yet

We have been talking about the iPhone. We haven't talked about the developer.

Our own developer-relations leads in Helsinki and London tell us that web developers — not handset developers, web developers — are beginning to build for Mobile Safari and treating Symbian and Windows Mobile as legacy targets. [10] Not because Symbian is technically worse. Because Mobile Safari runs the web they already wrote. At WWDC six weeks ago Apple did not announce a native SDK. It announced web apps as the SDK and shipped Safari for Windows the same day. [11], [12]

The twenty-eight-year-old building for the iPhone in July 2007 is the thirty-six-year-old running an engineering team in 2015. By then his team has spent eight years on Apple's documentation. They are not looking for a reason to switch to us. They are not looking for us at all.

Apple is not just selling a phone. It is recruiting the software developers who will define mobile for the next decade. [11] We have eighteen months. Probably less.

The Experience Is the Marketing

We do not need to tell Wired that the N95 has GPS.

We need a browser so good that the buyer reads his morning news on the train without opening a laptop. Today our browser reflows the desktop web one narrow column at a time. [13] That is the marketing. He shows the colleague at the next desk. The colleague buys the phone.

The One Number

Does the high-end buyer run his web life on our phone, or does he keep using his laptop and use our phone for voice? [14]

When the answer is "on our phone" — touchscreen good enough, browser fast enough, application ecosystem alive — the revenue per user follows. It always does when you get the product right.

The Decision

Everything in this memo — the platform review, the developer-relations rebuild, the touch-first UX programme — waits for one decision.

Someone in Espoo is currently deciding whether Multimedia runs as its own business, with its own P&L, its own R&D priority list, and its own brief to compete on experience. That person has not yet said yes.

So the question for this Board is simple:

Do we run Multimedia as a separate business from Mobile Phones — with its own P&L and its own strategic mandate — or don't we?

If yes: Board decision before end of Q3. Multimedia head reporting to the CEO. Platform decision for Multimedia made independently of Mobile Phones, by end of Q4.

If no: the cash engine continues to subsidise smartphone R&D pointed at the wrong product question. By end-2009 either the high-end tier has lost the developer ecosystem permanently, or the cash engine has lost its pricing power, or both.

Those are the two options. There is no third.

Let's get to work.

Nokia and the iPhone: The Memo Never Written (Marketing Canvas Method)

Page 2 — The Evidence Annex

[1] — Apple iPhone first-weekend sales

Apple disclosed at its Q3 fiscal 2007 earnings call on 25 July 2007 that the iPhone sold 270,000 units in its first thirty hours of US sale, against the partial quarter ending 30 June. AT&T disclosed at its Q2 2007 earnings call on 24 July that it had activated 146,000 iPhones over the same launch weekend, with the gap attributed to activation-server load on its side. Apple has publicly targeted 1 million cumulative iPhone sales by 30 September 2007 and 10 million by year-end 2008. Pricing: $499 (4GB) and $599 (8GB), both with a 24-month AT&T contract.

Apple Computer Q3 FY2007 earnings call, 25 July 2007 | AT&T Q2 2007 earnings call, 24 July 2007

[2] — N95 feature advantage over iPhone

The Nokia N95, on sale in Europe since March 2007 and in the United States via unlocked channels at €550, ships with: 5-megapixel autofocus camera with Carl Zeiss optics, integrated GPS, 3G/HSDPA radio, Wi-Fi, microSD expansion, full hardware keypad, Symbian S60 3rd Edition. iPhone first-generation ships with: 2-megapixel fixed-focus camera, no GPS, EDGE-only radio (2G), Wi-Fi, no expansion slot, virtual on-screen keyboard, no third-party applications. On a column-by-column feature comparison the N95 wins on six of eight commonly compared specifications. Engadget and GSMArena published direct comparisons in March–June 2007.

Nokia N95 product specifications, March 2007 launch | Apple iPhone technical specifications, June 2007 launch | Engadget product comparison, May 2007

[3] — Mobile Safari as a desktop-replacement browser

Mobile Safari on iPhone uses the full WebKit rendering engine — the same engine as desktop Safari — and renders the desktop web at full layout, allowing pinch-zoom and tap-to-zoom navigation rather than column reflow. Walt Mossberg's Wall Street Journal review of 26 June 2007 explicitly identified the browser as the iPhone's most disruptive feature, noting that it was the first mobile browser that did not require a separate mobile version of the site to be readable. The architectural choice (full WebKit + multi-touch) is the source of the developer-ecosystem implication addressed in entry [10].

Wall Street Journal, "Testing Out the iPhone," Walt Mossberg, 26 June 2007 | New York Times, David Pogue review, 27 June 2007

[4] — Nokia Multimedia segment average sales price

Nokia's Multimedia business group reported net sales of €7,877 million in 2006 on 39.0 million converged-device units, an implied average sales price of approximately €202. The N-series-tier individual ASP is materially higher (N95 unlocked at €550; N73 unlocked at €350); the segment ASP is suppressed by mix. The relevant comparison number for this memo is the segment ASP, since the strategic decision sits at segment level.

Derived — methodology: Multimedia 2006 net sales €7,877M ÷ 39.0M units = €202. Nokia Q4 and Full Year 2006 results release, 25 January 2007

[5] — Mobile data ARPU at the developed-market premium tier

Average revenue per user on the data component of a postpaid smartphone-tier subscription in the United Kingdom and the United States ranges approximately £30–£40 per month inclusive of voice and data bundles for the high-end consumer cohort, of which approximately €40 (≈£27) per month is attributable to data and content. Annualised €500. This number is the revenue stream the device sale enables and which the device manufacturer does not currently share in. The data-ARPU pool is the prize the iPhone is engineered to expand.

Derived from operator postpaid tariff disclosures, UK and US, June 2007 | Confidence: Q3 — trade tariff data, not a single named methodology

[6] — iPhone integrated user-experience features

The iPhone ships with: Mobile Safari (full WebKit web browser), the iPod application (integrated music player with iTunes synchronisation), Visual Voicemail (a carrier-software feature jointly developed with AT&T allowing non-linear inspection of voicemail), Mail, Maps (using Google Maps), Calendar, multi-touch capacitive screen. Apple's 9 January 2007 Macworld keynote and 29 June 2007 launch event identified the integration of these components, rather than any individual component, as the product proposition. Notably absent: third-party applications, MMS, copy-and-paste, document editing, expansion storage.

Apple Macworld keynote, 9 January 2007 | Apple iPhone launch event, 29 June 2007

[7] — Nokia communications framing the N95 against the iPhone

Nokia communications around the N95 launch and through May–June 2007 have emphasised the N95's feature superiority over the iPhone on metrics where Nokia leads (camera megapixels, GPS, 3G radio, applications support). The framing is reflected in trade-press coverage including Engadget, GSMArena, and Mobile Industry Review during this period. The strategic concern is not that the framing is factually wrong — it is correct — but that it accepts the comparison set on terms that disadvantage Nokia for the next ten years.

Confidence: Analyst inference from trade-press patterns May–July 2007. Not internally confirmed as a directive comms strategy.

[8] — Symbian as the assumed platform for the high-end tier

Nokia's published product roadmaps and Symbian Foundation governance documents show Symbian S60 3rd Edition as the platform for the current N-series and E-series, with S60 5th Edition (touch-screen capable) in early development for shipping units in 2008–2009. There is no publicly disclosed Nokia executive-level review of whether Symbian is the correct platform foundation for an experience-led €500–€700 device tier under conditions of touchscreen disruption, in either Q1 or Q2 2007 financial communications. The platform commitment for the 2008 product cycle is currently in formation.

Nokia Q1 2007 results materials, 19 April 2007 | Symbian Limited product roadmap disclosures, 2006–2007 | Confidence: Analyst inference — absence of disclosed review, not confirmed absence of internal review

[9] — Nokia 2006 segment operating profit disclosure

Mobile Phones business group: 2006 net sales €24,769 million; 2006 operating profit €4,100 million; 16.6% operating margin; total Nokia device volume 347 million units of which Mobile Phones absorbs the majority. Multimedia business group: 2006 net sales €7,877 million; 2006 operating profit €1,319 million; 16.7% operating margin; 39.0 million converged-device units. The two segments report similar operating margins on dissimilar revenue bases, dissimilar volume profiles, and dissimilar competitive conditions. The shared margin masks the structural difference in strategic position.

Nokia Q4 and Full Year 2006 results release, 25 January 2007

[10] — Developer ecosystem migration toward Mobile Safari

Insider intelligence — qualitative, not independently verified. Nokia developer-relations leads in Helsinki and London report informally that mid-2007 platform-choice conversations with web-application developers increasingly default to Mobile Safari as the priority mobile target, with Symbian S60 and Windows Mobile treated as legacy targets. The shift is partial and early; it is qualitative not quantitative; it is concentrated in the developer cohort building for the developed-market premium consumer (the same cohort the Multimedia tier targets).

Corroborated by external signals [11] and [12] below | Confidence: Insider intelligence; corroboration is two Q1-grade signals

[11] — Apple's developer-recruitment positioning at WWDC 2007

At the Apple Worldwide Developers Conference on 11 June 2007 in San Francisco, Steve Jobs and Scott Forstall presented web applications running in Mobile Safari as the iPhone development model, in the absence of a native software development kit. The framing was greeted with disappointment by attending developers and openly critiqued by independent commentators including John Gruber (Daring Fireball, 11 June 2007) for its substantive thinness. The salient strategic fact is not whether the "sweet solution" is technically sufficient — it is not — but that Apple has now framed Mobile Safari as the developer-recruitment surface for the iPhone, and the developer community is engaging with that framing rather than declining it.

Apple WWDC 2007 keynote, 11 June 2007 | Daring Fireball, "WWDC 2007 Keynote News," John Gruber, 11 June 2007

[12] — Apple ship of Safari for Windows, 11 June 2007

Apple released Safari 3 beta for Microsoft Windows on 11 June 2007, the same day as the WWDC keynote. The strategic purpose stated in Steve Jobs's keynote was to allow Windows-platform web developers to test sites against the Safari rendering engine — that is, against the engine the iPhone uses. This is a developer-recruitment infrastructure investment. It is not visible inside conventional handset-competition analysis. It is highly visible to the developer community Apple is targeting.

Apple press release, "Apple Releases Safari 3 Public Beta for Windows and Mac," 11 June 2007 | WWDC 2007 keynote

[13] — Mobile browser comparison: full rendering vs column reflow

The Symbian S60 browser used in Nokia N-series and E-series devices (including the N95) is itself built on WebKit but applies a column-reflow rendering strategy designed to optimise small-screen text legibility — pages are reformatted to a narrow column rather than rendered at the desktop-web layout. Mobile Safari on iPhone retains the desktop layout, allowing the user to zoom and pan rather than read reflowed content. The architectural choice is the source of the qualitative "real internet" claim that recurs in iPhone reviews. Mossberg's WSJ review of 26 June and Pogue's NYT review of 27 June 2007 both identified the rendering difference as the iPhone's most decisive product advantage.

Symbian S60 Web Browser documentation, 2006 | Wall Street Journal and New York Times product reviews, 26–27 June 2007

[14] — Multimedia segment revenue uplift arithmetic

The Multimedia segment generated €7,877 million in 2006 on 39.0 million units (ASP €202). If Nokia captures a 10–15% revenue share of the developed-market data-ARPU pool through commercial partnership with carriers (per-user services revenue, content distribution, application-store equivalent), and if the high-end share within Multimedia (~30% of units) is the addressable cohort, the incremental annual revenue is on the order of €700–€1,100 million by 2010 against the 2006 base. The figure is illustrative of the order of magnitude, not a forecast. The arithmetic depends entirely on the commercial-model decision the platform decision unlocks, and is therefore a downstream consequence of the Board decision identified in this memo, not an independent target.

Derived — methodology: 39.0M units × 30% high-end share × €40/month data ARPU × 10–15% capture rate × 12 months = €560M–€840M annualised; range widened to account for ASP-uplift effect on the device side. Sources: Nokia 2006 financial reports; UK/US operator tariff data. Confidence: Q4 — illustrative scenario arithmetic, not a forecast