Apple Is Facing Two Different Problems. Almost Everyone Thinks It's One.

What fifty years of archetype transitions reveals about the world's most valuable company — and why the diagnosis matters for every brand that has ever dominated its category.

Everyone is looking at the same evidence. Vision Pro shipped roughly 45,000 units in the 2025 holiday quarter — the quarter that is supposed to be Apple's strongest. Manufacturing had already stopped. Digital advertising for the product had been cut by more than 95 percent in its two biggest markets. Apple Television announced spatial computing as the next frontier. What the telemetry shows is a category that never formed.

At exactly the same time, Apple Intelligence — Apple's generative AI system — is widely characterised as late, incomplete, and outmanoeuvred. Google Gemini is already on devices. OpenAI has shaped the vocabulary consumers use to describe what AI on a phone can do. Apple's version of the story arrived after the category definition was written by someone else.

The consensus frames both as the same problem: Apple is missing the frontier. Vision Pro is one data point. Apple Intelligence is another. Both signal that the world's most valuable company — $416 billion in revenue, $112 billion in net profit, all-time records in fiscal 2025 — has somehow lost the ability to lead where technology is going.

The consensus is wrong about the most important thing.

Vision Pro and Apple Intelligence are not the same problem. They are mechanically different at the level of what caused them. They require entirely different responses. And treating them as one problem — which almost every analyst, journalist, and CMO currently does — produces wrong conclusions about both.

Here is what the framework reveals.

The operating system behind the audit

The Marketing Canvas Method classifies companies into nine strategic archetypes — think of archetypes the way you think of states of matter. Water, ice, and steam are the same molecule behaving differently under different conditions. The same company, under different market pressures, occupies genuinely different strategic postures with different capabilities and different ceilings. A move that works in one state fails in another. The molecule doesn't change. The behaviour does.

Each archetype is defined by three variables: where the company sits in its market cycle, how it creates economic value, and which lever it pulls to grow. Change one of those variables and you change the archetype — and therefore the entire set of moves available to the company.

Apple is currently operating as a Brand Evangelist (A3) — the archetype of a company that has built a loyal, deeply embedded tribe and is now running its extraction machine at full power within that base. Understanding what that means in practice requires understanding how Apple got there.

Six states, fifty years

Apple has run six of the nine archetypes in its history. No other company in the case library comes close. That is not a claim about Apple's strategic genius. It is a claim about what happens to a company that lives long enough through enough market transitions.

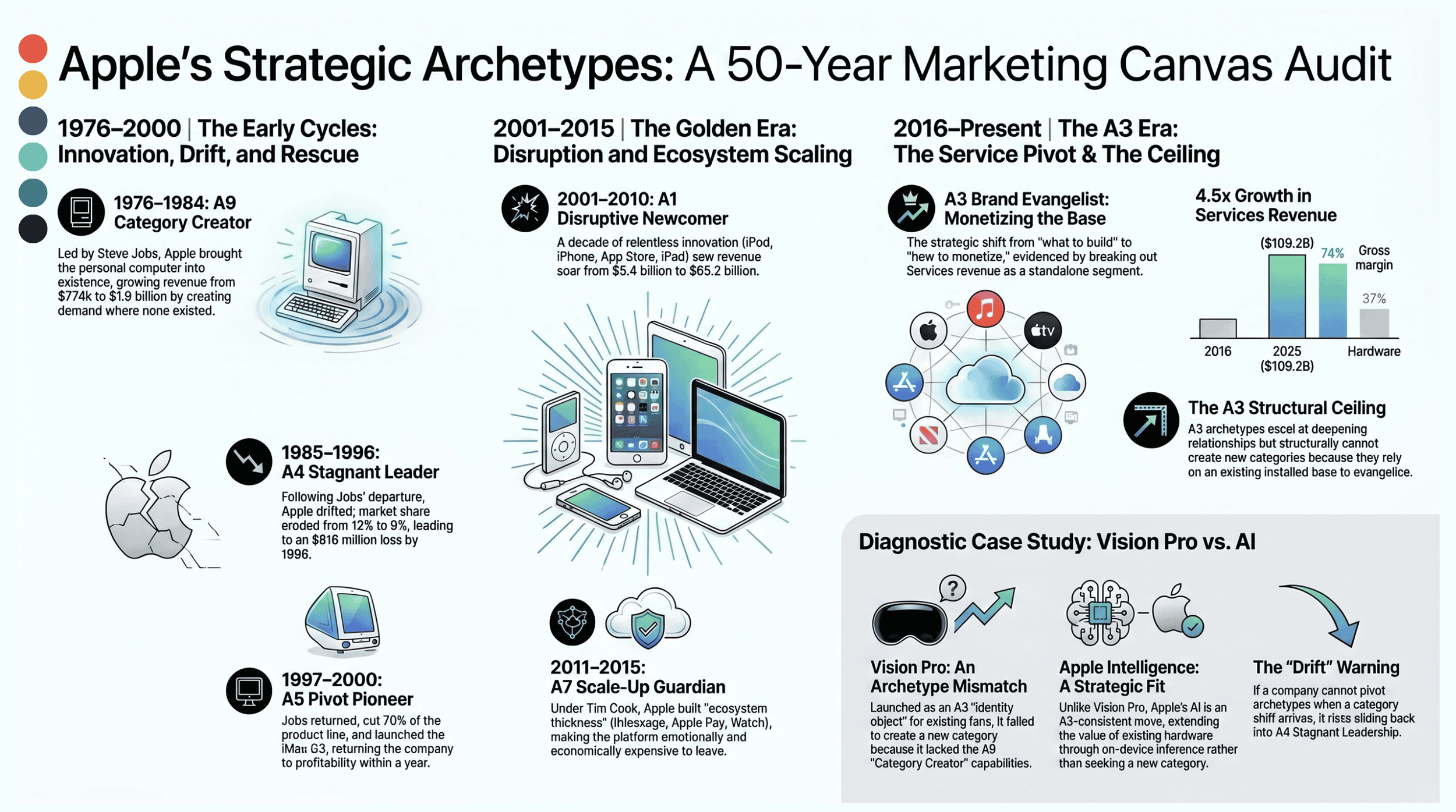

Phase 1 (1976–1984): Category Creator (A9). The personal computer as a consumer appliance did not exist before Apple. Apple had to create the category before it could compete in it. The "1984" Super Bowl commercial — no product on screen, nothing but the emotional position of liberation from conformity — is the canonical act of this posture. Apple was not competing for share in a market. It was building the arena.

Phase 2 (1985–1996): Stagnant Leader (A4). The board sided with Sculley over Jobs in May 1985. Jobs left in September. What followed was eleven years and three CEOs. Market share fell from 12 percent to below 4. The next-generation operating system Apple needed to survive — five years and hundreds of millions of dollars in development — was cancelled in 1996. The company reported losses large enough that analysts were modelling acquisition scenarios. This is the decade most people forget. It is also the most instructive, because it shows exactly what happens to a successful brand that loses the capability that made it successful — slowly, invisibly at first, then catastrophically. Financial statements were the last thing to confirm what the framework would have shown years earlier.

Phase 3 (1997–2000): Pivot Pioneer (A5). Jobs returned through the NeXT acquisition. He cut 70 percent of the product line in his first 120 days. He launched "Think Different" — not to sell a product but to rebuild the internal conviction that Apple was worth fighting for. The iMac followed. Three years from insolvency risk to sustained profitability. The compression was possible because Jobs' authority profile — returning founder, largest individual shareholder, absolute product veto — gave him latitude that no normally-appointed CEO survives. The recovery set a benchmark the method has not seen equalled.

Phase 4 (2001–2010): Disruptive Newcomer (A1) — the insurgent's archetype. iPod. iTunes Store. iPhone. App Store. iPad. Revenue from $5 billion to $65 billion in nine years. Apple's market capitalisation surpassed Microsoft's in May 2010. What the mythology around this decade obscures is the sequencing: each product built the platform for the next. iPod required iTunes. iTunes required the iTunes Store. The iTunes Store required the App Store relationship with developers. The App Store made the iPhone a platform rather than a product. The sequencing was not accidental, and its logic was not available to competitors trying to replicate individual products without building the underlying architecture.

Phase 5 (2011–2015): Scale-Up Guardian (A7). Cook became permanent CEO. The strategic mission shifted from disrupting incumbents to protecting the ground already taken. The walls Apple built during this phase — iMessage, FaceTime, AirDrop, Continuity, Apple Pay, Apple Watch — were not locks. They were not contracts. They were convenience so profound it became structural. A household with five Apple devices, all speaking to each other through layers of shared infrastructure, faces a switching cost that no competitor can eliminate by offering a better individual product.

Phase 6 (2016–present): Brand Evangelist (A3). The transition marker is specific. In January 2016, Apple began reporting Services as a standalone revenue segment. That accounting event signalled a strategy shift: the question was no longer what to build next, but how to extract more value from what was already built. Services revenue has grown from roughly $24 billion that year to $109 billion in fiscal 2025. The extraction machine is running at extraordinary efficiency.

Every one of those five transitions was triggered by a CEO change. Not a product launch. Not a market event. A CEO change. The incoming leader's implicit reading of Apple's context — which market phase, which value model, which revenue lever — determined the archetype more reliably than any strategy document. That pattern is not coincidental. It is the mechanism.

A second pattern runs through the same six phases, quieter than the first. The weakest capability across every Apple era has been the same one: the company's systematic capacity to listen for market signals it was not already expecting. Jobs' personal intuition substituted for this capacity in Phases 1 and 4 and left no apparatus behind when he departed. The iPhone 6 big-screen pivot in 2014 is the single visible moment in the six-phase record when Apple responded to an external signal that contradicted its own orthodoxy — and the installed base that resulted from that pivot is the reason the extraction machine has $109 billion to work with today. Vision Pro and Apple Intelligence will read, in the case library ten years from now, as the same capability gap surfacing four decades on.

A9Category Creator

A4Stagnant Leader

A5Pivot Pioneer

A1Disruptive Newcomer

A7Scale-Up Guardian

A3Brand Evangelist

Every transition was triggered by a CEO change — not a product launch, not a market event. Each successful transition pre-built the next archetype's capabilities during the previous phase. The exception is Phase 2, the only phase Apple did not exit by design — and the decade Apple nearly died. The current question is whether Apple's seventh archetype is being prepared during the sixth.

The diagnosis

Here is what the Canvas reveals about Apple's current posture that the revenue numbers cannot.

Brand Evangelist (A3) is built for one thing: deepening the value extracted from an existing base. Every measurement the Canvas uses to check whether A3 is working — engagement depth, emotional connection, values coherence, proof base, influencer reach, user lifetime — shows Apple scoring at or above the required thresholds. The tribe is embedded. The retention metrics are the strongest Apple has ever recorded. Services revenue at $109 billion is the extraction machine's output, not its ceiling.

One reading sits quietly alongside this strength. The values dimension that anchors tribal identity — the privacy position, the environmental commitments, the creator-empowerment promise — is at target, but at target under external pressure Apple does not control. Epic Games. The European Commission's Digital Markets Act. The right-to-repair coalition. None of these, alone, moves the score. Together, they hold it exactly on the line. A Fatal Brake sitting at target under active pressure is not a gap. It is the signal that arrives before a gap.

Brand Evangelist (A3) is not built for creating new categories. These are not the same capability. They cannot be acquired by investing more budget or hiring more talent into the current posture. The gap is architectural.

This is what Vision Pro is telling you, if you read the signal correctly.

When Apple launched Vision Pro in February 2024 at $3,499, the product had no resolved answer to the question every consumer implicitly asks at the moment of purchase: what specific problem in my life does this solve, that I recognise needing solved? The job of spatial computing — whatever it turns out to be — did not exist as an established demand before the product arrived. No market behaviour indicated that people were actively hiring products to fill this role. Apple had to create the category and the product simultaneously, which is the definition of Category Creator (A9) work. That archetype has a completely different operating system from Brand Evangelist (A3). Category Creator (A9) requires building the job-to-be-done and the product that delivers it at the same time, pricing them for first-adopter recruitment rather than tribe stimulation, and spending years on market education before commercial validation arrives. A3 runs none of those routines. It runs the extraction machine — and the extraction machine is exquisitely optimised for serving a job that already exists, not for creating one that doesn't.

Forty-five thousand units in the holiday quarter is not a number produced by an archetype executing category creation. It is a number produced by an archetype that does not have category-creation in its configuration, attempting to perform it anyway.

The counter-example: why Apple Intelligence is not the same problem

Apple Intelligence looks like the same frontier failure. The narrative says: Apple is behind in AI the same way it is behind in spatial computing. The framework says something different.

The job of using large language model capabilities on existing devices is not absent. It is everywhere. People are actively hiring products to do this job right now, on hardware they already own, through applications they use every day. Generative AI adoption has outpaced the historical growth curves of PCs and mobile phones. The demand signal was detectable, growing, and unambiguous — long before Apple's version reached market.

Apple's on-device processing approach is not a philosophical position. It is a technically grounded architecture that research validates as superior on the dimensions that matter most for this specific job: privacy (the data never leaves the hardware), latency (real-time response without a cloud round-trip), cost (no data-transmission bottleneck as inference scales), and scaling (decentralised local processing bypasses the structural limits of hyperscale data centres). The architecture is not the problem.

The problem is timing. Apple's delivery delay on personalised Siri features allowed Google and OpenAI to define the category's vocabulary and consumer expectations before Apple's version was fully available. When Apple Intelligence ships at full capability, it will arrive into a market that already knows what AI on a phone is supposed to feel like — and Apple will need to make the case that its version is worth reconsidering. That is a harder narrative position than arriving first. But it is a fundamentally different problem from Vision Pro's.

Vision Pro needed a job that did not exist. Apple Intelligence is late to a job that is already everywhere.

One of those problems requires archetype capability that Brand Evangelist (A3) does not have. The other requires delivering a product and building a narrative around a validated technical differentiation. These are not interchangeable. Every analyst who treats them as the same "frontier failure" is recommending solutions to one problem as answers to the other.

MCM - Apple's Strategic Archetypes

Three questions for your next strategy review

First: On which of your frontier bets does the job-to-be-done already exist? Separate your pipeline into two columns. In the first column: initiatives addressing a job that is already happening, already growing, already hiring products. In the second: initiatives that require your company to define the job and build the product simultaneously. The first column lives inside your current archetype's capability set. The second column requires capabilities you may not have. Know which column each bet is in before you allocate the budget.

Second: Is your company building the structural requirements of the next archetype while the current one is still profitable? Every successful Apple transition pre-built the next archetype's foundations during the current phase — before the transition was forced. Phase 5's ecosystem-thickening built what Phase 6's extraction machine required. Phase 3's positioning work built what Phase 4's disruption required. The only phase that failed to do this preparation was Phase 2. Phase 2 is the decade Apple nearly died. The preparation does not appear in this year's financial statements. It competes for capital with initiatives that do. The historical record is the argument for funding it anyway.

Third: When your board next discusses CEO succession, are you asking the archetype question? Every Apple archetype transition was triggered by a CEO change. Every incoming CEO produced an archetype, consciously or not. The board that appoints a successor is selecting the company's next strategic posture. The nature of the successor — which market phase their instincts are calibrated for, which value model their decision-making reflects, which revenue lever their capital allocation will pull — determines the next archetype more reliably than any succession framework that does not ask these questions.

The question that isn't settled

Apple's next 24 to 36 months will test something the case library has not yet documented: whether a Brand Evangelist (A3) can execute a planned transition to the next archetype from a position of operational strength — without a crisis forcing the move.

Every prior Apple transition was either crisis-triggered (1997, twelve weeks from insolvency) or market-forced (Cook's appointment when Jobs' health required it). The 2026 moment is different. Apple's performance is too strong for an externally forced transition. The internal case for change — the argument that record revenue and record profit coexist with a structural ceiling that financial statements cannot see — has to be made on the strength of the archetype diagnosis alone. That is the hardest version of the move. Organisations that are succeeding do not naturally redirect resources toward capabilities they do not yet need.

Three signals over the next twenty-four to thirty-six months will tell you which direction the trajectory has broken. First: whether Vision Pro's second-generation product ships at mass-market pricing with a resolved customer job — the evidence that spatial computing entered Disruptive Newcomer (A1) territory rather than staying a category that never formed. Second: whether on-device Apple Intelligence matures into measurable user-behaviour shift — developer adoption, feature coverage, the kind of telemetry that confirms the architectural bet was right. Third: whether iPhone revenue as a share of total revenue trends below forty-five percent — the structural marker that Services has crossed from supplementary to primary, and the archetype has deepened rather than drifted. Any two of these converging in the strong direction point toward the Hermès pattern — decades of Brand Evangelist (A3) stability, extraordinary financial performance, no transition required. Any two converging in the weak direction point toward drift into Stagnant Leader (A4), the archetype Apple already knows intimately from 1985 to 1996. The third becomes the tiebreaker.

The CEO succession will be the upstream signal. Based on the pattern across five prior transitions, the nature of the successor will tell you more about Apple's next archetype than any product roadmap or strategy presentation that follows it.

Six archetypes in. The ceiling is visible. Whether Apple clears it — and how — is the open question.